For the markets, February was a period involving the consolidation of the levels achieved since the beginning of the year, although some corrections did occur. The month was characterised, as usual, by the inflation data and the meetings of the central banks, as well as the subsequent speeches of their members to emphasise that the battle against inflation is yet to be won.

Global growth

In view of the forecast of weaker growth, there is the risk of a recession in the United States and the Eurozone so as to reduce inflation to the target levels in a sustainable manner. Even so, the market is placing increasing importance on the possibility of a soft landing.

In China, the zero-Covid policies, the challenges facing the property sector and the higher commodity prices led to very weak growth in 2022.

However, this growth is expected to improve from now on, due to the support for the policies and the re-opening of the economy, although there are downside risks, given the slower rise in exports due to weaker global demand.

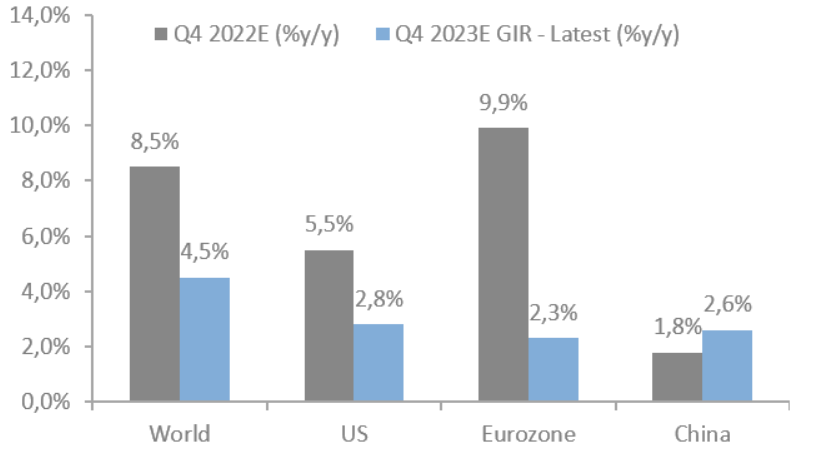

Inflation

Inflation is expected to slow down during 2023, but the short-term risks of higher inflation remain.

Inflation forecasts for 2023 compared to 2022

Source: Goldman Sachs Asset Management

Core inflation appears to have begun to slow down in the United States, driven by the lower prices of goods as the supply chain problems ease due to weaker demand.

However, for inflation to fall towards the target sustainably, we need to see a slightly weaker labour market, moderation in pay growth towards 3%-3.5% and greater weakness in house prices and new-lease rentals, which are reflected in the official rental inflation rates after a certain time lag.

Monetary policy

It seems like the central banks will have to continue with their restrictive monetary policies in an environment of positive growth and high inflation, even more so after the recent strong macro-data in the United States and the trend towards disinflation that isn’t progressing as fast as expected.

Both the Fed and the ECB raised their rates (by 25 bps and 50 bps, respectively) at their meetings in early February, as the markets had expected.

The markets are setting the maximum rate at 5.1% in the USA in the second quarter of 2023; however, rate cuts totalling 35 bp are expected by the end of the year, in contrast to the Federal Reserve’s projection of envisaging no cuts for 2023 and a rate standing at 4.1% by late 2024.

Equity

After the sharp rises, the forecast for 2023 is more cautious in terms of equity.

In keeping with the macro-environment, corporate fundamentals have also been adjusted; the profit margin has moved lower in line with BPA’s expectations.

The fourth-quarter profits have been weaker and profit growth has been negative in the main sectors. Companies have lowered their future expectations, reflecting the higher costs of materials and labour and the lower demand.

Within the context of greater uncertainty, together with the expected weakness of company fundamentals, the return/risk ratio is veering downwards.

Fixed income

Fixed income has priced in the higher final interest rates, making this asset attractive despite its short-term volatility.

Persistent inflation and central banks with aggressive monetary policies can keep the real rates at high levels for longer.

The risk of having long lengths doesn’t offset the returns in this environment, in which good returns can be obtained with average lengths.