In recent weeks we have seen the market momentarily forget about inflation to focus on fears of a possible entry into recession in both Europe and the United States. This situation has caused the assets most sensitive to the economic cycle to experience significant falls in anticipation of this possible recession.

1. What repercussions would a recession have on the value of major financial assets: equity and fixed income?

Quite small and clearly smaller than the price impact shown by both traditional fixed-income assets (between -10 and -15% in the year) and equity assets (between -15% and -25% in the year). In the case of the first benchmark asset, the impact is neutral to positive, as recessions are usually linked to a fall in expectations of rate hikes and a flattening of the curve, which ultimately means a lower discount rate for bonds and principal to be received in the future. The negative effect obviously comes from corporate bonds, because higher quality corporate bonds tend to compensate for falling government curves by widening credit spreads, while in the issues of more speculative or indebted companies, credit spread widening is generally higher than curve compression; this may cause this sub-asset to fall in recession scenarios. The reality, however, is that this particular sub-asset has already partially discounted a recession by accumulating average falls of 20% in both Europe and the United States and we think that, in any case, it is an asset that is beginning to be attractive by paying IIRs of over 7% in EUR and 9% in USD.

What about equities? Again, the impact is less than what is being expected. After all, the value of a company is nothing more than the sum of all the cash flows it will generate in the future; that is, standardised earnings taken to the present day. If we take into account that historically the market pays around 15 times forward returns, we can infer that one or even two bad earnings years (on a long-term upward trajectory) have little impact. In normal recessions, business profits do not usually fall by more than 20-30% with rapid recoveries. Even if we assumed two years with depressed global profits of 30%, the equivalent impact on the intrinsic value of companies would be less than 6%, assuming a conservative 10% discount rate.

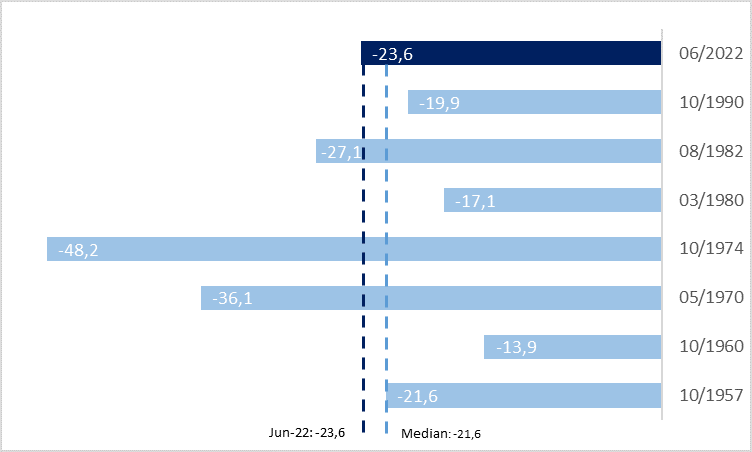

Thus, the impact of a normal recession on the valuation of major financial assets has little to do with the falls from highs to lows that the S&P 500 index has undergone and are shown below. In fact, what we see is that when the United States has entered a recession, as a result of a tightening of monetary policy and not by an external shock or the bursting of a bubble, the accumulated falls in these indices are on average slightly lower than those we have already experienced in the current year.

And we are talking about a normal recession, as we think that, in the event of a recession (which is not a sure thing either), it should be mild given that both the financial health of families and companies remains good with debt levels clearly lower than those of the great financial crisis of 2008.

Graph 1: S&P 500: falls from highs to lows during recessions induced by a tightening of monetary policy.

Source: Goldman Sachs Asset Management. 07/2022

2. History tells us that far from reducing exposure to financial assets, we should start increasing it

Although a complex macroeconomic scenario like the one we are experiencing might lead us to think that it is better to stay out of the financial markets, the reality is that if we do a review of historical data, this strategy indicates high probabilities of failure. This year we have entered a bear market, which has accumulated falls of more than 20% from highs to lows. If we review all the times that this has happened in the S&P 500 index since 1945, we observe that two years after marking this -20% on average the profit has been 33% (double the average return in two-year periods for this index). That’s not to say the market can’t fall further, but it does indicate that based on history being invested now clearly increases the chances of getting good returns in the future.

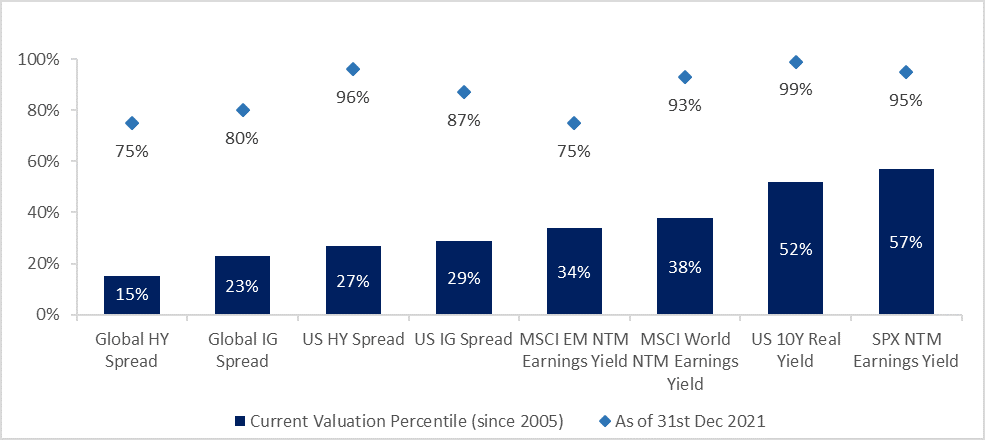

Does this mean we have already seen minimums? We do not know. What we do know is that both historical data and, more importantly, favourable valuation starting levels indicate that medium-term returns (3-5 years) from current levels should be at least satisfactory. As we see below, almost all of the assets shown are trading below their historical average, which is usually the most important element in generating good returns in the medium term.

Graph 2: Percentage of valuation of different financial assets today vs. the closing of 2021 with data from 2005

Source: Goldman Sachs Asset Management. 07/2022

#MoraBancExperts