IT stocks outperform, irrespective of interest rates

Some of you will be familiar with the Miniágora client events that organize MoraBanc Asset Management, at which we talk about markets and investment opportunities. The latest edition took place last week, under the title Stranger things.

We are keen on TV series, as you can see; and this one specifically was a kind of homage to 1980s science fiction classics, such as Spielberg’s Close Encounters of a Third Kind or E.T. The title refers to recent phenomena, such as the closing down of short-volatility products (see my last editorial) or the collapse of the bitcoin. However, I believe there are far stranger things going on, like the possibility of a trade war in the event of an escalation in the tariffs introduced recently by the US on steel and aluminium (a couple of months ago, Trump also placed tariffs on washing machines and solar panels, albeit relatively unnoticed).

It seems odd, after more than two decades of globalisation (taking as reference the creation of the World Trade Organisation in 1995) that has boosted the growth of emerging economies (yet without harming that of developed economies – just look at the S&P500), that for the first time we are now having to worry about the geopolitical and macroeconomic implications of a return to protectionism. I am not sure who exactly is going to be hit by the tariffs on industrial metals, because the US allies may well be exempt, and those not so allies, like China, don’t export much steel anyway, which suggests that the headlines about a trade war look very exaggerated. What worries me more is the investigation that the US administration has started into the supposed theft of intellectual property rights by China; this could lead to far more damaging protectionary measures, for both China and, as a consequence, for the US, most probably for the technology sector and maybe even for the whole market. When the intellectual property hits the headlines (replacing steel), a correction considerably more violent than that in February shouldn’t be a surprise, in my view.

In the meantime, the IT sector keeps on rising (YTD +10% vs. S&P +3%), which has made me (a sector bull a year ago) distinctly sceptical. Technology stocks are going up, despite:

1) the fact that their earnings are not growing much more than those of the S&P (tax cuts improved the earnings outlook for other sectors), which means there is no reason for them to outperform; and

2) the drop in treasuries (10 year yield now at 2.90%).

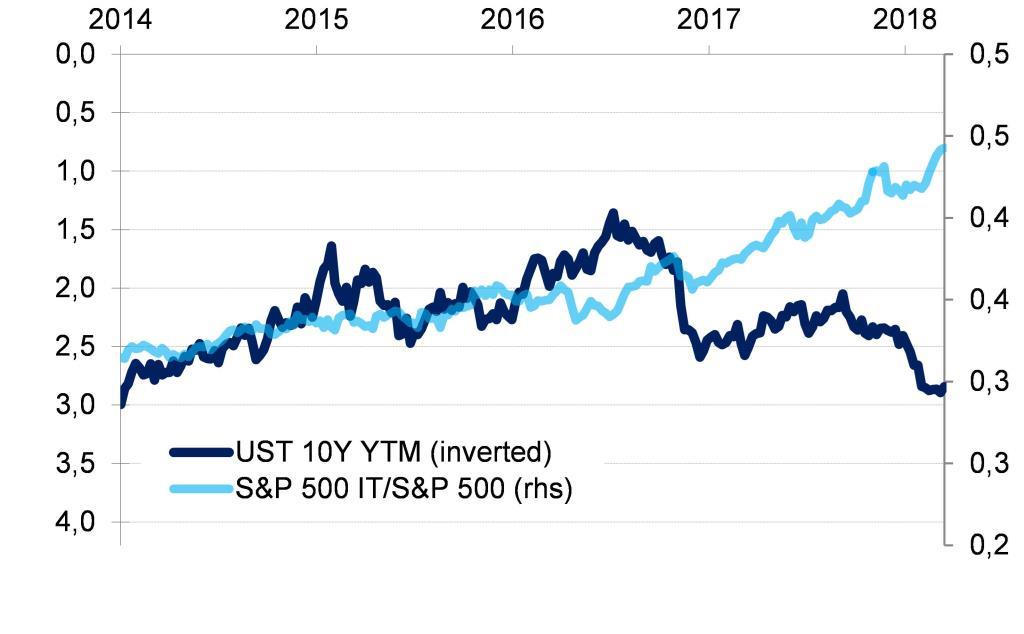

Many market gurus believe that the normalisation of interest rates will put an end to the tech rally. The argument is that companies with high-growth profiles and no dividends are long duration assets that ought to outperform when rates are falling, and underperform when they are rising; but the likes of Facebook, Amazon, Apple, Netflix, and Google (FAANG) appear to be unstoppable irrespective of the direction of interest rates. Stranger things indeed.