Central banks and inflation have been front and centre in the first half of the year, against a backdrop not seen for decades. Inflation has continued to be the main issue, driven by tight labour markets, supply chain dynamics that have cut the supply of many key materials, and geopolitical tensions. In the United States, the Federal Reserve has embarked on a tightening of monetary policy to control price pressures. The other influential central banks in the global economy are also ready to tackle inflation, albeit at a different pace than the Federal Reserve.

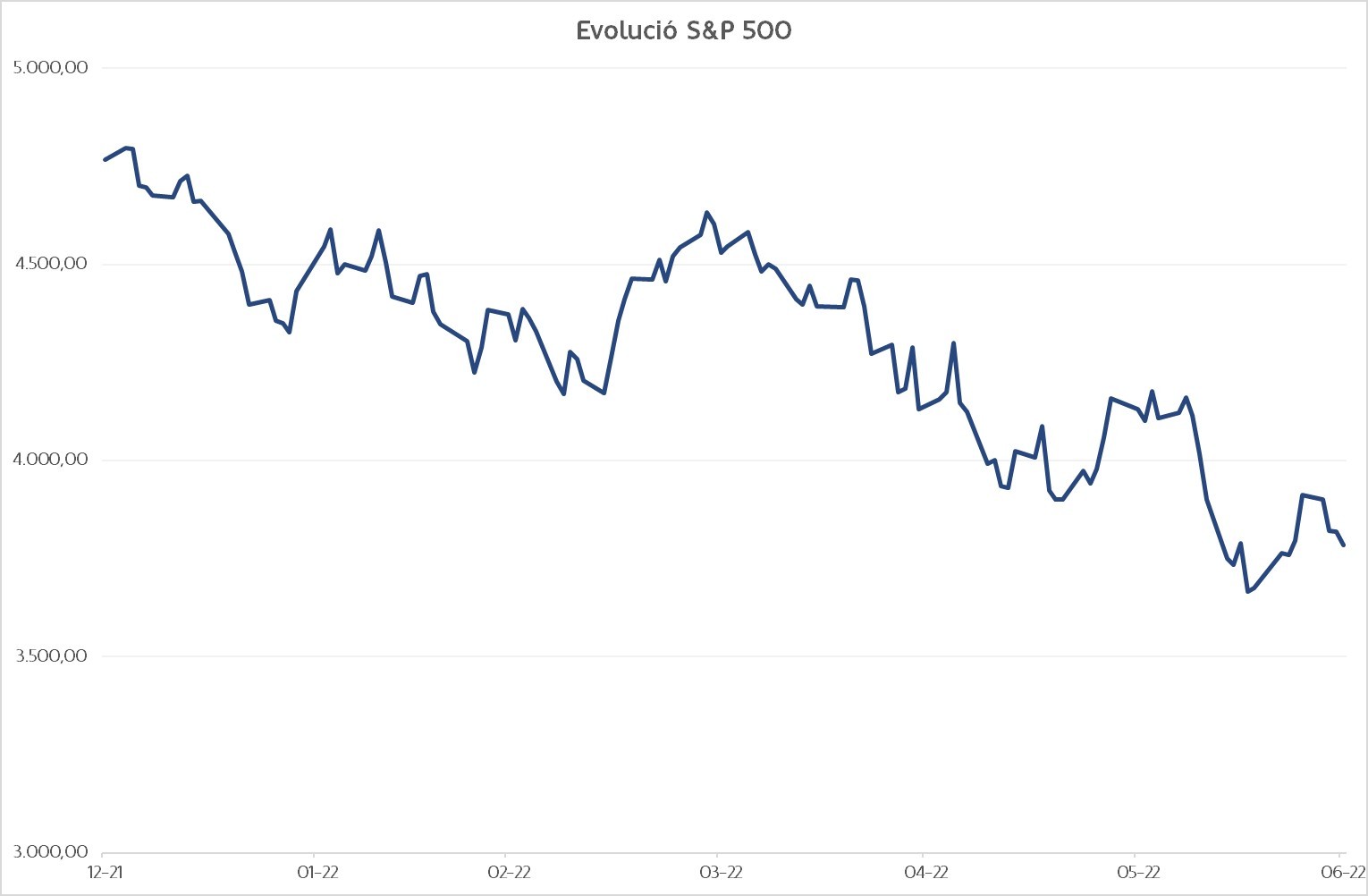

1. S&P 500 closes out worst first half in 50 years

The worldwide economic slowdown and central banks’ aggressive raising of interest rates have hurt global stock market indices. One of the most affected areas has been the United States. The S&P 500 fell -20.6% during the first half of the year, wiping out the profit of 2021. It is the worst start for this index since 1970, although the rest of American indices, particularly the Nasdaq 100 technology index, which recorded losses of -29.5% in the first half of the year, are not far behind.

Graph 1: S&P 500 index performance as of 30 June 2022

Source: Bloomberg

2. Global growth slowdown

Financial conditions in the United States have tightened by 180 basis points over 2022, which is expected to weigh on GDP growth by 2 basis points until the end of the year. Although headwinds such as import normalisation and the reopening of the service sector after the pandemic could cushion the impact, GDP growth in the US is expected to slow to 2.4% in 2022. In China, the authorities need to carefully consider the balance between their zero-COVID policy and the weakness of the housing sector and external demand, which would set the pace of its GDP development.

3. USA: personal consumption expenditure (PCE) deflator

The personal consumption deflator is the Fed’s main inflation benchmark, and it is currently remaining at levels not seen since 1982. This means that the Fed is justified in continuing to raise rates, with the market expecting that they will be in the 3.25%–3.50% range by the end of this year. This May, the PCE has stabilised at +6.3%, the same as the previous month, but slightly better than expected. Moreover, personal spending, which fell -0.4% in May, is now reflecting the impact of inflation and higher financing costs on consumption and therefore fuelling doubts about economic growth.

Table 1: Performance of PCE and personal spending from December 2021 to May 2022

Source: Bloomberg

#MoraBancExperts