In the second half of October, inflation continued to show signs of global strength as fears of recession grew in the investment community. Given the situation, the ECB acted again with a rate hike of 75 basis points, and this is not expected to be the last of the year. On the other hand, the corporate results of the third quarter so far helped to reduce the losses accumulated this year in the stock market indices.

1. Evolution of the growth-inflation relationship

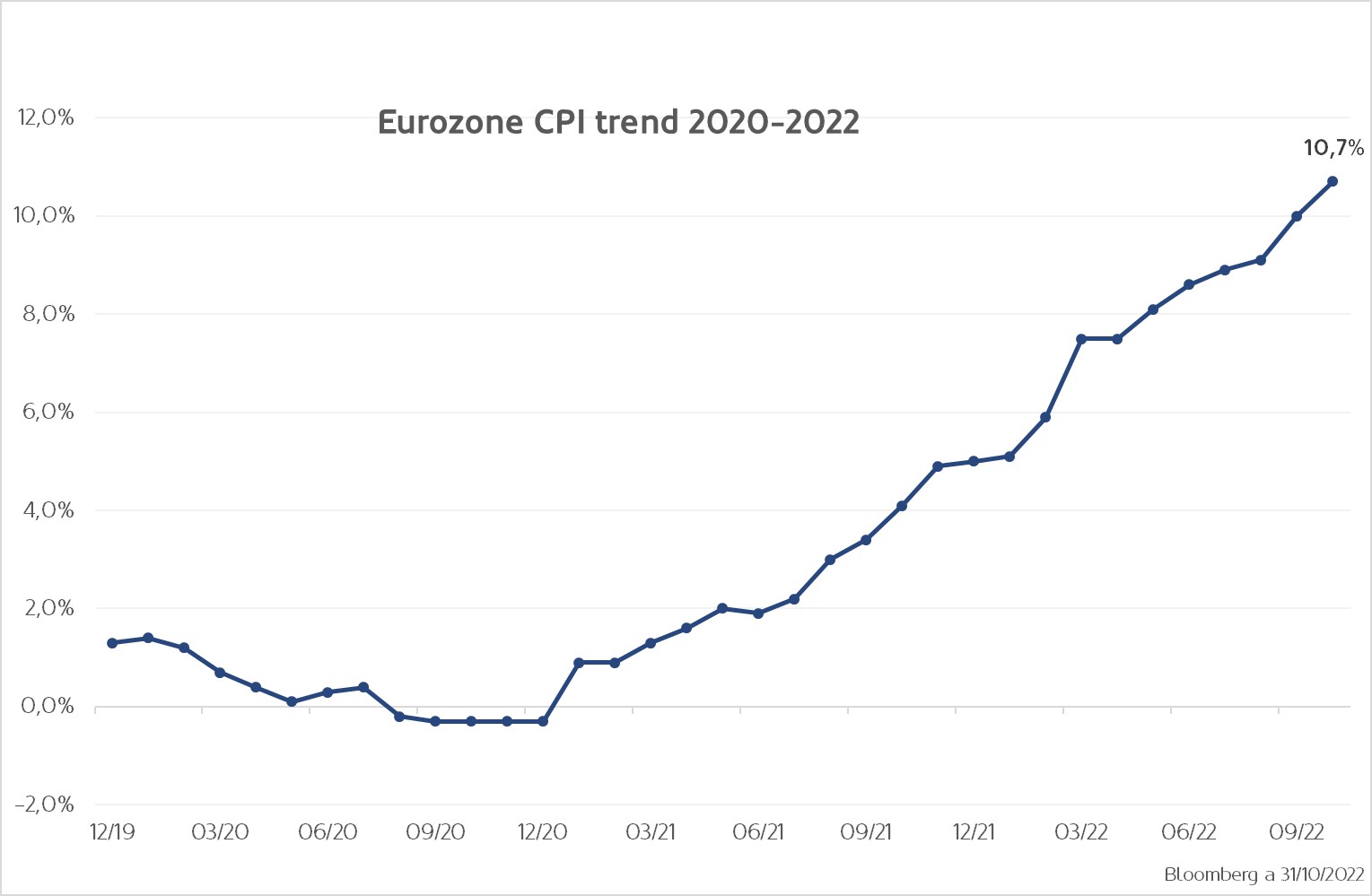

Eurozone inflation in October rose to an estimated 10.7% year-on-year, well above expectations of 10.2%. Core inflation reached 5% y-o-y, in line with expectations. For the time being, prices are not giving any respite, with energy as the component that is weighing most heavily on the European economy. The full breakdown by component will be published by Eurostat on Thursday 17 November.

Graph: Eurozone CPI trend 2020-2022

The first effects of this high inflation and tight monetary policy are already being reflected in economic indicators such as GDP, which in the case of the Eurozone decelerated to 0.2% in the third quarter of 2022 from the previous figure of 0.8%.

All but three countries showed positive growth, led by Italy, Portugal and Lithuania. Overall, real GDP in the Eurozone is now 2.1% above its pre-pandemic level.

2. ECB raises the price of money again

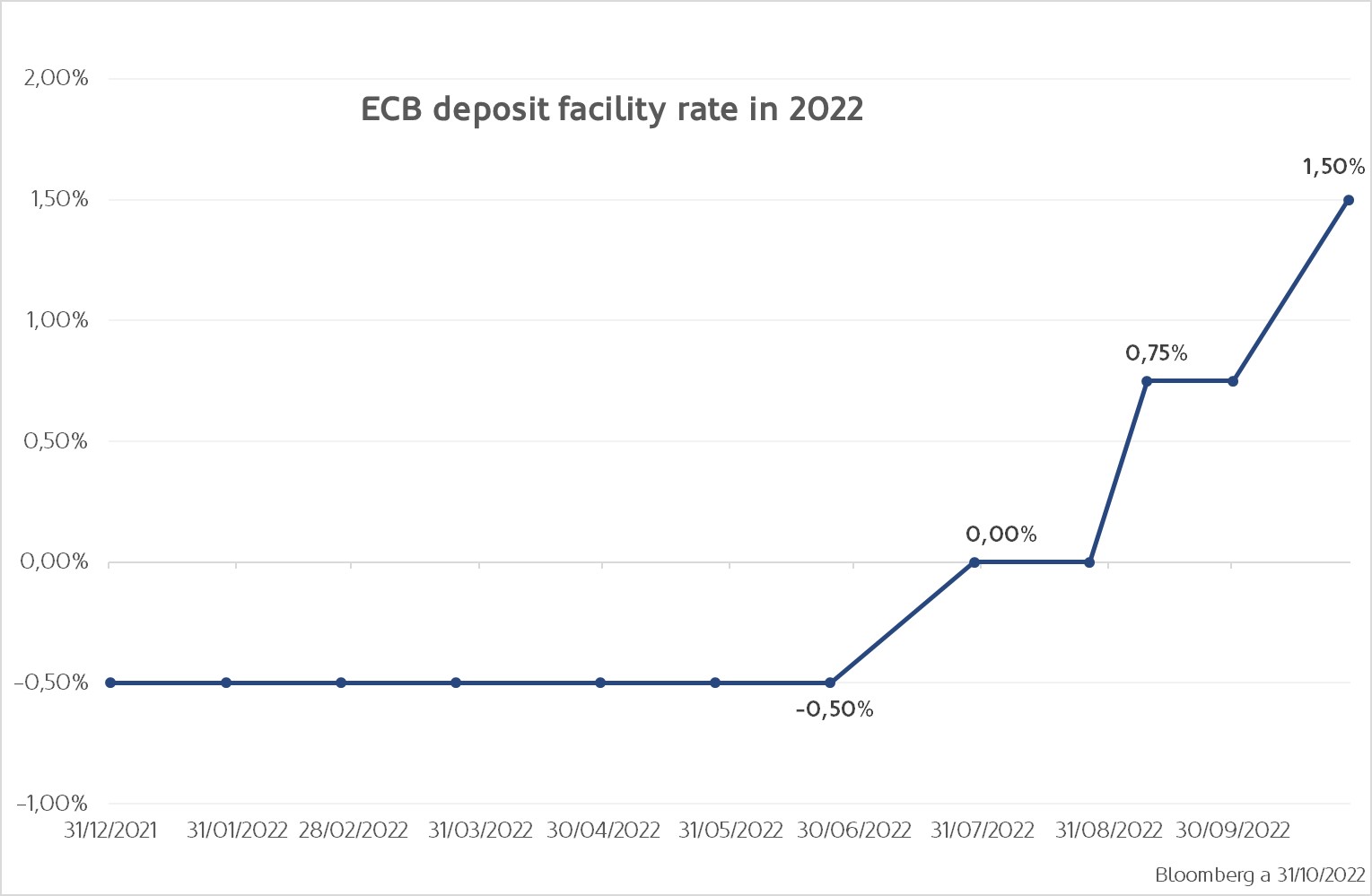

The European Central Bank raised interest rates by 75 basis points, bringing its benchmark deposit rate to 1.50%, the highest level since 2008.

The hike was widely discounted by the market, but in her speech Lagarde noted that “substantial progress has been made in the withdrawal of accommodative monetary policy”. As inflationary pressures continue, the Bank leaves the door open to further rate hikes, but suggests that it is preparing the ground for a slowdown in rate hikes as the risk of recession increases.

Gràfic 2: Taxa de facilitat de dipòsit del BCE en 2022

On the other hand, various risks facing the old continent were discussed, such as further increases in energy prices as a result of the geopolitical conflict with Russia, the likely increase in the unemployment rate as a consequence of the economic slowdown and the depreciation of the euro as a pro-inflationary factor.

3. Positive first impressions of business results

In the second half of October, equity markets managed to gain around 6% in both Europe and the United States, partly due to quarterly results that, despite the economic slowdown, continue to surprise on the upside. However, the movement has not been without volatility as in some cases market prices have abruptly picked up disappointing reports; here the weakness of the US technology sector is particularly noteworthy. We enter November with the second half of the companies still to report.

Another bullish catalyst was the release of US third quarter GDP, which showed above-estimated growth of 2.6%. These events, together with the stabilisation of the political situation in the UK, offset concerns about inflation, the tightening of monetary policy and the increased likelihood of recession.