Market outlook September 2023

6 October de 2023

The month of September has been marked by stock market corrections, both in Europe and the United States, and by the strong rise in fixed income interest rates. A tougher message from the Federal Reserve, at the last meeting in September, together with the fears caused by a possible US government shutdown due to the notorious debt ceiling limit, caused sales in the main stock market indexes.

In monetary policy, we seem to be in the final phase of interest rate hikes, and the market already has its sights set on the upcoming falls, which are not expected until well into 2024.

Macroeconomics and monetary policy

A divergent growth trend is observed, on the one hand, in the United States and Japan, which they seem to be resisting, and on the other hand, Europe and China are slowing down significantly. It is also observed that in general the deflation process is continuing, but this does not rule out that there may be some upticks in inflation (this was noted in the August data due to the impact of the increase in commodity prices).

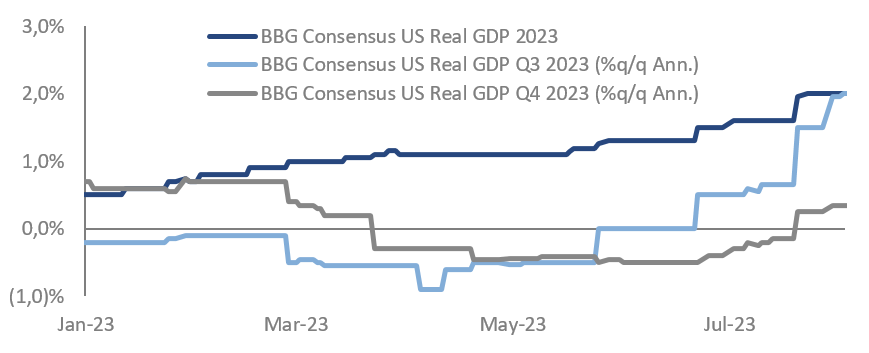

United States: activity data are stable, but are weakening slightly. A deterioration in Consumer Confidence is observed. Advanced indicators suggest weaker growth in the future, even though the rate hike seems to benefit because of the possibility that the American economy can manage to control inflation without going into recession or, in any case, only a very mild recession. No rate cuts are expected this year, and it appears that the labour market is easing gradually.

Strong US data prompts notable revision of GDP growth expectations

Source: Bloomberg and Goldman Sachs Asset Management

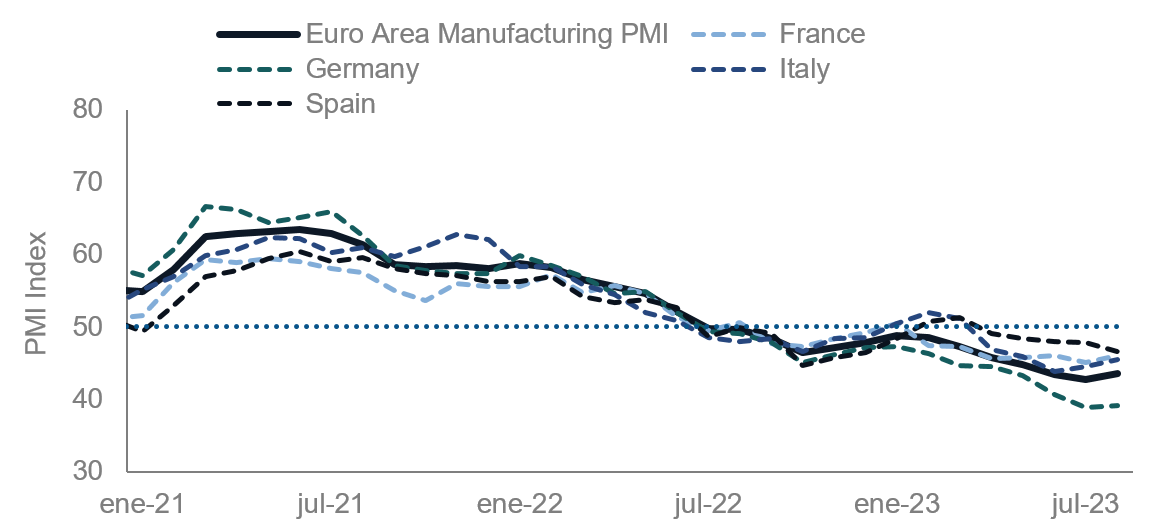

Europe: more moderate growth is expected this year and is weakening, mainly affected by the slowdown of the German economy. There will be a more accentuated economic weakening in the future, with a very high risk of recession after the data seen in the summer. It seems that the ECB could be at the height of its rate hikes. This is how the institution conveyed it at its September meeting, and we do not expect to see rate cuts until the second half of 2024.

The weakness of the euro zone continues, especially in Germany

Source: Bloomberg and Goldman Sachs Asset Management

China: the property sector crisis and the weakness of the export sector continue to hamper growth. The government’s stimulus policy has been too limited so far and further stimulus is expected.

Japan: domestic demand continues to hold up. The Bank of Japan eased its monetary policy slightly in July and maintained it in September. The policy may begin to be reversed over time.

Vision by assets

As for the equity market, the resistance shown in the latest activity data in the United States has been reflected in a positive dynamic of business earnings. The economic activity data from Europe, on the other hand, has been particularly weak. Weakening demand in China and the slowdown in the global manufacturing sector exert an additional pressure on European figures for its cyclical or value side. This environment lets us have more positives in developed markets in relation to emerging markets, with a preference for the large capitalization companies. Europe must be prudent, since the most highly leveraged and cyclical sectors are the most vulnerable to slower growth and tighter credit conditions.

The positive inertia of the markets could still continue in the short term, supported by possible interest rate cuts by the Central Banks. However, taking into account expectations of weaker grow and a possible weakening of business results, we prefer to maintain a cautious positioning in equities, above all with regard to Europe and China.

With respect to fixed income assets, yields trended higher in August and September. US rates look attractive at current levels, taking into account the scenario of an economy that is at an end-of-cycle phase, near the peak of the rate hike cycle and already in high levels of real profitability. In Europe, inflationary pressure is higher, but the risk of a slowdown is also greater for this economy. In this scenario, it is difficult to think that the ECB can continue to raise rates, so we consider it interesting to build a portfolio at these levels.

As for credit, the tightening of lending rules by banks and the expected slowdown in growth make us more cautious on the worst rated credit, especially for the United States.