Market outlook – February 2024

6 February de 2024

The month of January started with uncertainty in the main markets, and as the month progressed, optimism prevailed in the financial markets, which allowed the main stock markets to close on a high. Thus, the Eurostoxx 50 rallied by almost 3% and Wall Street closed with a slightly more moderate rise due to how poorly received the words of the chairman of the Federal Reserve on the last day of the month were, while delaying expectations of lower type and causing widespread falls. Thus, the S&P 500 closed the month with a rise of 1.60% and the Nasdaq with 1%.

The macroeconomic data were the main protagonists in January, with inflation figures, US labour market data and GDP standing out as the highlights. January highlighted again the strength of the North American market and the weakness of the Eurozone. Central banks caught the attention of analysts at their meetings at the end of the month.

The central banks

The European Central Bank was the first to speak, while keeping the rates unchanged for the third consecutive meeting, as expected. It was indicated that they expect to keep rates at restrictive levels as long as necessary, awaiting the evolution of macroeconomic data. The meeting of the Federal Reserve took place at the end of the month, maintaining the rates in the range of 5.25%-5.5%, not to the surprise of analysts. The surprise was the delay in rate cuts in the short term. The organisation pointed to the fact that “the economic situation is still very uncertain”, that “it is very attentive to inflationary risks”, and does not withdraw the threat to raise rates further if “risks arise that hinder” the lowering of inflation.

Fixed income

Government profitability fell slightly in January. The US 10-year Treasury closed trading below 4% and the German bond with the same maturity closed at 2.20%, far from recent highs. The same trend was seen in peripheral countries: Spain’s 10-year bond traded at 3.10% levels and the Italian bond at 3.7%.

Forecasts by geographic areas

United States

Growth in the US economy is expected to moderate from the robust levels observed in the last quarter of 2023. The decline in inflation continues, but may be more volatile in the short term. The market is awaiting the Fed’s first interest rate cuts, and adds a 90% chance that the first will happen in May.

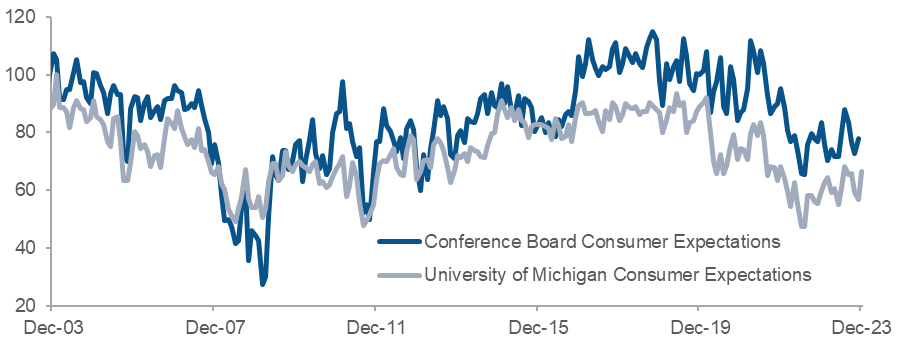

Consumer confidence in the United States shows signs of recovery

Europe

The income of households should be helped by a strong labour market and ever-lower inflation, but the monetary policy will increasingly affect growth. Fiscal policy will be tightened slightly and companies are likely to face some downward pressure on margins. The impact of these cross currents should lead to moderate growth in the coming quarters.

Japan

Solid growth is expected driven by a strong labour market, improved business confidence and accommodative monetary policy. The most important factor is that the economy is supported by a cycle of positive feedback, involving rising inflation and nominal growth expectations on the one hand, and falling real returns on the other.

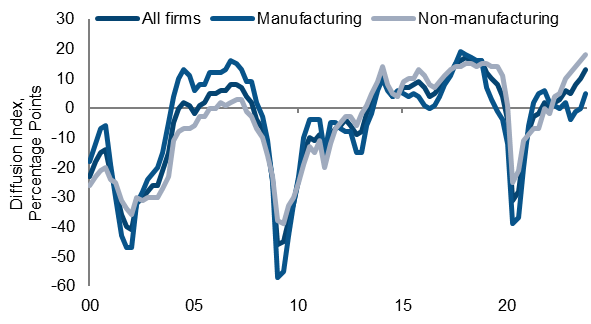

TANKAN survey in Japan that measures economic and commercial activity

China

With the property sector and exports in difficulty, the overall growth momentum remains weak. Households remain risk averse and sales of new homes are unlikely to have bottomed out yet.

The main risk to growth continues to stem from low business confidence due to state interventionism and the uncertainty about possible legislative changes. The goal of 4.5%-5% GDP growth is likely to be achieved in 2024.